Pricing Continuously Funded Everlasting Options

The recent “Everlasting Options” paper by White, D. et al has introduced a new type of financial derivative, Everlasting Options, inspired by the funding-fee-based paradigm introduced by BitMEX for the perpetual futures. Perpetual futures have become extremely popular since their inception and brought to the industry a new category of derivatives, i.e. the derivatives with positions maintained by regularly paying funding fees. Everlasting Options adopt this paradigm to options markets and have the potential to avoid the rolling issues and largely reduce the degree of liquidity fragmentation.

Everlasting Options work similarly to Perpetual Futures: a long position is maintained by paying funding fees to a short position. However, in the case of everlasting options, the funding fee is charged as (MARK-PAYOFF). Considering that theoretically MARK should always be higher than PAYOFF, the funding fee should always be positive (i.e. long positions always pay short positions). For options, (MARK-PAYOFF) has a specific financial significance — time value. Therefore, the mechanism of maintaining an everlasting option position has a very obvious financial significance too: option buyers pay the time values of the options associated with specific funding periods.

By means of the no-arbitrage argument, White has proved a pricing framework for funding-fee-based perpetual derivatives:

where F is the payment frequency and P(tᵢ)is the price of the regular option with expiration of tᵢ (REGPRICE of tᵢ).

We are especially interested in adopting this pricing method in DeFi scenarios, where funding is usually accrued on a per-block basis. This corresponds to very large F. Mathematically, the cases of large F are more convenient to be treated as F ⟶∞. When F converges to infinity, this leads to a special funding style — continuous funding. That is, the funding fee that one long contract should pay one short contract is accrued continuously. This is similar to how interest is accrued for continuously compounded interest rate.

Let’s denote the funding period as T (e.g. 1 day) and payment interval as ∆t=T/F (e.g. 1 hour if F=24). Then we can rewrite the formula above. Note that tᵢ=i∆t= iT/F and i=Ftᵢ/T, we have

When F ⟶∞, ∆t⟶0, we have

And the summation converges to an integral

Specifically, for everlasting call and put options, we have

If we price C(t) and P(t) by the classic Black-Scholes pricing formula with interest rate ignored:

where

N= CDF of the normal distribution

S= spot price of the underlyer

K= strike

𝝈 = volatility of S

then we can prove the following pricing formula for the continuously-funded everlasting options.

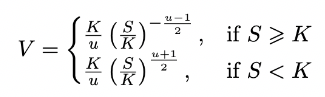

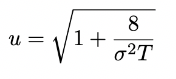

Pricing Formula

Let’s divide Cᵉᵛᵉʳ and Pᵉᵛᵉʳ into intrinsic value and time value:

We can prove that the call and put options at the same strike have the same time value TimeValue𝒸ₐₗₗ=TimeValueₚᵤₜ=V, given by

where

The details of derivations are laid out here.

About Deri Protocol

Deri Protocol is a decentralized protocol for users to exchange risk exposures precisely and capital efficiently. It is the DeFi way to trade derivatives: to hedge, to speculate, to arbitrage, all on chain. This is achieved by liquidity pools playing the roles of counterparties for users. With Deri Protocol, risk exposures are tokenized as NFTs so that they can be imported into other DeFi projects for their own financial purpose. Having provided an effective on-chain mechanism to exchange and hold risk, Deri Protocol has minted one of the most important blocks of the DeFi infrastructure.